Form 990-T Instructions

Quick Links:

E-File Your Form 990-T with Tax990!

- Supports 990-T Schedule A

- Includes major supporting forms

- Built-in error check for accurate returns

- Complete guidance at each stage of filing

How to Fill Out your 2025 Form 990-T: Step-by-step instructions

- Updated March 05, 2025 - 2.00 PM - Admin, Tax990

Form 990-T is an annual information return filed by tax-exempt organizations to report unrelated business income and tax liabilities to the IRS.

It is filed by the organizations who file Form 990, 990-EZ or 990-PF and have an unrelated business income of $1000 or more.

The due date to file Form 990-T for the trusts defined in sections 401(a) and 408(a) is the 15th day of the 4th month after the organization's accounting period ends. For other organizations, the deadline is the 15th day of the 5th month from the accounting period’s ending.

This article provides step-by-step instructions on how to fill out your Form 990-T.

Instructions to complete Form 990-T

Form 990-T comprises 5 parts. Here are step-by-step instructions on how to fill out the details on

each part.

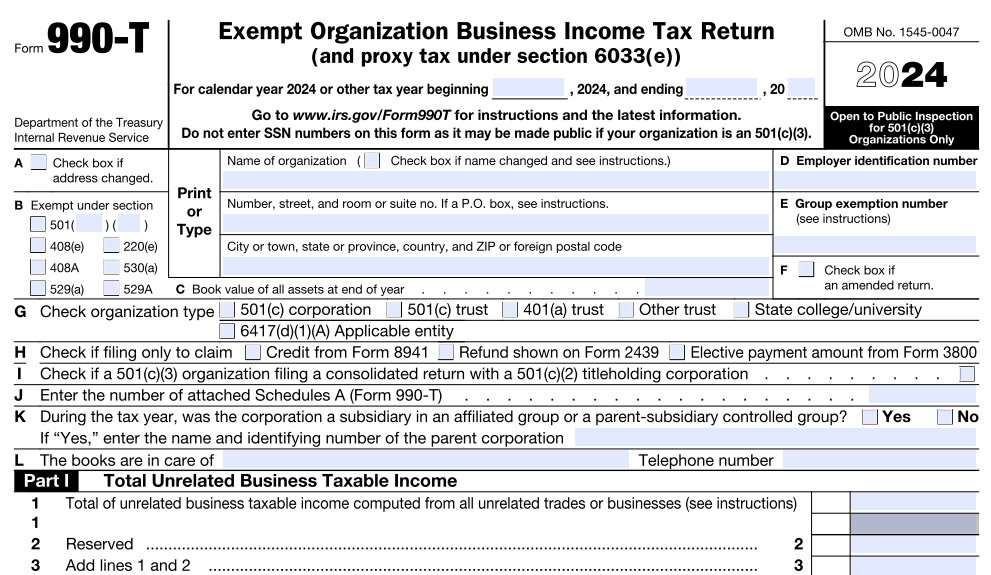

Basic Information About Your Organization:

The IRS requires you to provide the Name and Address of your organization. After that, provide the details mentioned below:

A. Check if your organization’s address is changed

B. Mention the section under which the organization is exempt

501( ) ( )

408(e)

220(e)

408A

530(a)

529(a)

529A

C. Enter the book value of the assets at the end of the year

D. Employer identification number (EIN)

E. Group Exemption Number

F. Check if you are filing an amended return

G. Select the type of your organization

501(c) corporation

501(c) trust

401(a) trust

Other trusts

H. Mention the purpose of filing

To claim credit from Form 8941

To claim a refund shown on Form 2439

I. Check if your organization is described under section 501(c)(3) and filing a consolidated return with a 501(c)(2) titleholding corporation

J. Mention the number of Schedule As attached

K. If the corporation was a subsidiary in an affiliated group or a parent-subsidiary controlled group, check “Yes” and enter the parent corporation’s name and identifying number

L. Provide details about the organization’s bookkeeper.

Part I - Total Unrelated Business Taxable Income

In this part, the IRS requires you to provide complete details about the taxable income generated by your organization from various unrelated businesses.

-

Line 1 - 3:

Enter the total amount of income generated through one or more unrelated businesses or trades by your organization.

Add the first 2 lines and enter the total.

Note:

Currently, The IRS requires you to leave line 2 blank.

-

Line 4:

Enter the amount paid by your organization to Section 170(c) governmental organizations for charitable purposes (contributions or gifts) and the unused contributions carried over from prior years (if any).

-

Line 5:

Enter the value of total unrelated business taxable income before net operating losses by subtracting line 4 from 3 to derive.

-

Line 6 and 7:

Mention the amount of net operating losses arising in tax years that started before January 1, 2018, or the total amount of unrelated business income (whichever is smaller).

Subtract lines 6 and 5 and enter the total of unrelated business taxable income before specific deduction and section 199A deduction.

-

Line 8 - 10:

Enter the allowable specific deduction (smaller of $1,000 or the local unit’s gross unrelated

business income).If you are filing Form 990-T for a trust that has unrelated business income, you may be allowed a QBI (Qualified Business Income) deduction under section 199A.

Note:

Refer to Form 8995 instructions to determine whether you meet the requirements for the

QBI deduction.Add lines 8 and 9 to derive and enter the Total Deductions.

-

Line 11:

Subtract the total deductions from line 7 and enter your organization’s unrelated business

taxable income.

Part II - Tax Computation

This part involves tax computations based on the values you reported in the first part.

-

Line 1:

Multiply the amount of unrelated business taxable income by 21% (0.21) and enter that value. (For organizations taxable as corporations)

-

Line 2:

If you are filing for a Trust, you should choose whether the income tax amount on unrelated business taxable income was computed from a Tax rate schedule or Schedule D (Form 1041).

-

Line 3:

If you have failed to include the required information regarding lobbying expenditures on your Form 990 or failed to provide notices to the members regarding their share of dues, you just pay Proxy tax (Not applicable for Section 501(c)(3) organizations).

Multiply the aggregate amount not included in the notices described earlier by 21% to calculate the proxy tax.

-

Line 4:

Enter the value of tax amounts that aren’t reported on any other specific lines.

-

Line 5:

This line is applicable only for Trusts. If your trust is liable for an alternative minimum tax on certain adjustments and tax preference items, attach Schedule I (Form 1041), and enter any tax from Schedule I on this line.

-

Line 6:

Enter the tax on non-compliant facility income (Hospital Organizations).

-

Line 7:

Add lines 3, 4, 5, and 6 to either line 1 or 2 and enter the total value.

Part III - Tax and Payments

In this part, you are required to provide details about total taxes, credits, payments, and overpayment.

-

Lines 1a - 1e:

Enter the amount of Foreign Tax credits and attach Form 1118 if you are filing for a corporation and Form 1116 if filing for a Trust.

Also provide details about General business credit (attach Form 3800), Credit for prior year minimum tax (attach Form 8801 or 8827), and Other Credits.

Add all the credits and enter the amount of Total Credits.

-

Line 2:

Subtract total credits from the total value of Tax computation and enter that amount here.

-

Line 3:

Enter the other amounts due and check the applicable box.

Form 4255 - Recapture of investment credit

Form 8611 - Recapture of low-income housing credit

Form 8697 - Interest due under the look-back method

Form 8866 - Interest due under the look-back method for property depreciated under the income forecast method

Other - If the previous boxes do not apply. Also, attach a statement showing the computation of each item included.

-

Line 4:

Enter the value of Total Tax, including tax previously deferred under section 1294.

-

Line 5:

Enter the value of the current installment of Section 965 tax liability paid in Form 965-A (Trust) or Form 965-B (Corporation).

-

Line 6 (a - g):

Provide details about all the tax payments.

Overpayment credited from the prior year

Enter the total estimated tax payments made. Include your organization’s share if it’s the beneficiary of a trust that makes a section 643(g) election.

Enter the amount of tax deposited with Form 8868.

Report the amount of tax withheld on unrelated business taxable income from U.S. sources through a trade or business conduct outside the United States.

If your organization is subject to backup withholding in error, you can claim credit for the amount. Enter the claim amount here.

If you are filing for a section 501(c) organization, you can file Form 8941 to claim the refundable small employer tax credit for a percentage of certain health insurance premiums paid on behalf of the employees. Enter the claim amount here.

Check the applicable box and provide details about other credits, adjustments, and payments

- Form 2439 - Credit from a regulated investment company (RIC) or a real estate investment

trust (REIT) - Form 4136 - Credit for federal fuel taxes.

- Other - For other credits.

- Form 2439 - Credit from a regulated investment company (RIC) or a real estate investment

-

Line 7:

Add all the values entered on Lines 6a - 6g and enter the Total Payments.

-

Line 8:

Check if your organization owes a penalty amount to the IRS, and attach Form 2220.

Note:

You can also attach Form 2220 if the annualized income or adjusted seasonal installment method is used or your organization is a “large organization” computing its first required installment based on the prior year's tax.

-

Line 9 - 11:

Enter the value of Tax dues if the value of total payments is smaller than the sum of lines 4, 5,

and 8.Enter the value of Overpayment if the value of total payments is larger than the sum of lines 4,

5, and 8.Enter the amount of overpayment you want to credit to the estimated tax of the next tax year.

Part IV - Statements Regarding Certain Activities and Other Information

In this part, you must report your organization’s activities and other information.

-

Line 1:

Mention if your organization had an interest in or signature or other authority over a financial account in a Foreign country. If “Yes”, attach FinCEN Form 114.

-

Line 2:

Mention if your organization is involved in any money or property transfer to a foreign trust (directly or indirectly. If “Yes”, attach Form 3520.

-

Line 3:

Report the amount of tax-exempt interest received or accrued, if any.

-

Lines 4 and 5:

Provide details about the NOL(Net Operating Loss) carryovers from prior tax years.

-

Line 6a and 6b:

Mention if your organization has changed its accounting method and has described the change in its 990 form or Form 1128. If “NO”, provide an explanation.

Part V - Supplemental Information

You can use this part to provide an explanation for the last question in the previous part or any other questions from other parts of the form.

Signature and Paid Preparer:

Your Form 990-T must be signed by the president, vice president, treasurer, assistant treasurer, chief accounting officer, or by any other officer of your organization.

If your 990-T return is prepared by a paid preparer, provide their details in this part.

Additional Filing Requirements for Form 990-T:

The organizations that file Form 990-T should also attach Form 990-T Schedule A with it to report the income and allowable deductions for each unrelated trade or business that they have reported on their main form.

For each unrelated business reported on Form 990-T, a separate Schedule A must be attached.

Make your 990-T Filing Simple and Quicker with Tax 990!

By offering various helpful features, the IRS-authorized e-file provider Tax 990 offers you an ideal way to securely e-file your Form 990-T.

With our Form-Based filing option, you can enter the required data directly on your Form 990-T.

- Based on the data you enter, our system will auto-include Form 990-T Schedule A for free.

Our Internal Error system reviews your completed form for any errors to ensure accurate returns.

Using our Reviewers and Approvers feature, you can invite your organization’s board members to review and approve your form.

We have a Dedicated Customer Support team available via live chat, phone, and email to assist with your questions.

Steps to file your Form 990-T:

Follow these steps to e-file your form 990-T with Tax 990:

Step 1

Add Organization Details

Either enter your organization details manually or let our system import the required details from the IRS using your EIN.

Step 2

Choose Tax Year

Tax 990 allows you to file Form 990-T for the current and the prior tax years. Select the tax year for which you need to file Form 990-T and proceed.

Step 3

Complete Form 990-T Details

Using our Form-Based filing process, enter all the required information on to your form.

Step 4

Review your Form Information

After providing all the required information, review the summary of your form and make changes

if required.

Step 5

Transmit directly to the IRS

Once you review all the information, you can transmit your Form 990-T to the IRS.